The atmosphere surrounding Obamacare, which was seen as a symbol of U.S. healthcare policy, is becoming tense.

There are analyses suggesting that the number of enrollees could drop significantly.

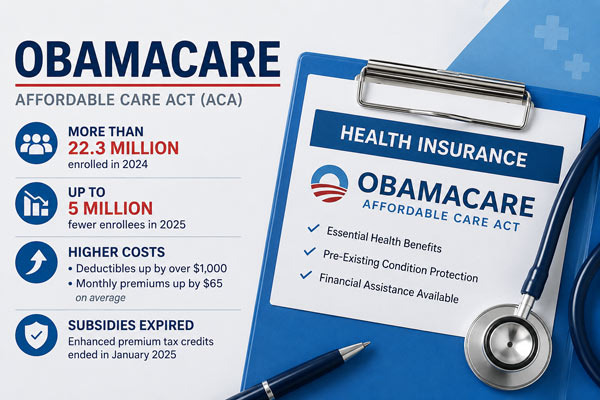

Last year, there were about 22.3 million enrollees, but this year, projections indicate that the number could fall to around 17.5 million.

This means a decrease of nearly 5 million, which is more than 20% of the total.

The key to this change is ultimately money. During the pandemic, the government covered a significant portion of premiums, allowing many people to maintain insurance at relatively low costs. However, as this support ends, the average deductible has increased by over $1,000, and monthly premiums have also risen by about $65 on average.

While this may not seem like a large amount, the burden feels much heavier for households. Especially for family enrollees, this increase is likely to be felt even more acutely.

The problem is that this burden is concentrated on a specific class. Low-income individuals can still receive some subsidy benefits, making it relatively sustainable for them.

On the other hand, the middle class finds itself in a precarious situation. Their income is slightly too high to qualify for support, yet they are in a range where the premiums become increasingly burdensome.

As a result, this class is likely to see the highest rate of dropouts. In fact, the current projections for decreased enrollment cite middle-class dropouts as a major cause.

Looking at this trend, one naturally wonders, "Is this system reaching its limits?"

However, upon closer examination, it is difficult to make such a definitive statement. The ACA was not designed as a perfect system; rather, it is a 'compromise model' that adds government intervention to an existing private insurance structure.

Therefore, for the policy to be sustainable, government support is essential. Some view this as a process of normalizing the artificially low cost structure that has been in place.

Another important point is the response of insurance companies. There are analyses suggesting that the market has already anticipated this change to some extent and has reflected it in pricing.

As a result, it is possible that next year will not see the same sharp increase in premiums as this year, but rather a more stabilized trend. Of course, this does not guarantee that the number of enrollees will rebound sharply. Ultimately, the core issue returns to 'how much can people afford?'

Realistically, the structural problems inherent in the U.S. healthcare system cannot be ignored. In a situation where medical costs continue to rise, there are clear limits to simply lowering premiums. Unless this structure is addressed, similar issues are likely to recur regardless of the policies implemented.

Therefore, some voices are increasingly calling for reforms aimed at lowering healthcare costs rather than merely expanding subsidies.

In the end, the current situation is closer to being "not a complete failure" but rather "in a state of being tested." The decrease in enrollment is certainly a warning sign, but it could also serve as an opportunity for policy adjustments. How the government redesigns the subsidy structure and what pricing strategies insurance companies adopt will be key variables that determine future trends.

At this stage, what is certain is that Obamacare is not over; it has reached a point where it needs to recalibrate its direction.

USALATU

USALATU

Always Flowing, That's All |

Always Flowing, That's All |

PPAP Pineapple Pen |

PPAP Pineapple Pen |

Mina Kim |

Mina Kim |

Cheese Hill Restaurant Exploration |

Cheese Hill Restaurant Exploration |

Everything Students Can Do |

Everything Students Can Do |

RV Samuel's Dad |

RV Samuel's Dad |

Tracking 60 Minutes News |

Tracking 60 Minutes News |

My Town My Way Blog |

My Town My Way Blog |

What can make money? |

What can make money? |  Sunshine Blog |

Sunshine Blog |  rockets |

rockets |  Holey Moley |

Holey Moley |  U.S. Supreme Court Judge Kim |

U.S. Supreme Court Judge Kim |  Soy Angelino |

Soy Angelino |  Cali M Law Group |

Cali M Law Group |  nixxon |

nixxon |  Yellow Snowman |

Yellow Snowman |  Shintongbangtong Shin Naerin James Park |

Shintongbangtong Shin Naerin James Park |  The Emperor Must Grow |

The Emperor Must Grow |  cloudyday |

cloudyday |  Heart Ticker |

Heart Ticker |  USA Business News |

USA Business News |  Best Frozen Yogurt |

Best Frozen Yogurt |  General Knowledge Blog |

General Knowledge Blog |  mistic |

mistic |  Univ Student |

Univ Student |