Many people believe that after 10 years of self-employment, they will qualify for Social Security benefits.

This is indeed true. If you have 40 credits, or 10 years of payment history, you are eligible for benefits.

However, it's important to understand that qualifying and the actual amount you receive are two very different matters.

Listening to stories from fellow Korean self-employed individuals, many feel reassured, thinking, "I've worked for 10 years, so I'll get my benefits later."

But this is only half true. I also ran the numbers while doing business in Georgia and was shocked by the amount I found.

Social Security benefits are calculated by the SSA based on a measure called AIME.

This is based on your average monthly income over your lifetime, with the key point being that it reflects income for a maximum of 35 years.

If you only worked for 10 years, the remaining 25 years will be calculated as having zero income. This structure significantly reduces the benefit amount.

Another important aspect is the reported income. Self-employed individuals often report lower net income to reduce taxes.

For example, if you report around $30,000 each year, it may seem beneficial in the short term to lower your self-employment tax.

However, this amount directly affects your benefit calculation.

If you calculate it, assuming you reported a net income of $30,000 each year for 10 years, your total income would be $300,000.

Dividing this by 35 years and then by 12 months gives an average monthly income of about $714.

Based on this amount, even if you start receiving benefits at age 67, you would get around $650 per month.

Annually, that's about $7,800. Considering whether you can live on this amount leads to a troubling conclusion.

In contrast, employees who have reported income for over 30 years often receive between $1,800 and $2,000 per month. The difference is significant.

Therefore, self-employed individuals need to approach this strategically.

First, rather than simply reporting low net income, it's necessary to adjust your reporting with long-term retirement benefits in mind.

Calculating the amount you will receive later is more important than just reducing taxes now.

Second, actively utilizing retirement accounts like SEP-IRA or Solo 401(k) is essential.

Self-employed individuals can save a substantial amount while receiving tax benefits, so missing out on this is a loss.

Third, it's advisable to check your spouse's Social Security record as well.

In some cases, it may be more advantageous to base your benefits on your spouse's record.

In conclusion, being self-employed means you have freedom, but you also bear all the responsibility.

Social Security is merely a minimal safety net, not a system that guarantees your retirement.

Thinking that you're prepared just because you have 40 credits is risky.

Living on $650 a month is difficult in the current U.S. economy, especially in large cities where it is very insufficient.

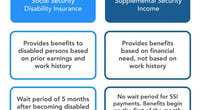

Many are confused, but sometimes the low-income assistance programs can provide better benefits than Social Security at $650.

For example, SSI is paid when income and assets fall below certain thresholds, with a maximum of about $943 for individuals in 2024.

However, SSI has asset limits and is reduced if you have other income, while Social Security is based on your own record and is paid for life regardless of assets.

In terms of sheer numbers, SSI may seem better, but you must consider the asset limits and conditions, which can vary based on individual circumstances.

Ultimately, preparing for retirement requires looking at future realities rather than immediate benefits. It's important to start calculating and preparing now.

celion78 |

celion78 |

USA Hyundai Kia |

USA Hyundai Kia |

Information on Area Codes in the Americas |

Information on Area Codes in the Americas |

Angeles Choi |

Angeles Choi |

Samttugi Grasshopper Noodle |

Samttugi Grasshopper Noodle |

Sunny Mom |

Sunny Mom |

Georgia Springcamp |

Georgia Springcamp |

moonshine 7 |

moonshine 7 |

Tiger Milk Foam Research Institute |

Tiger Milk Foam Research Institute |

Canvas Pro Blog |

Canvas Pro Blog |  Oh my Julia |

Oh my Julia |  4 Runner x100 |

4 Runner x100 |  My Carmen |

My Carmen |  Tony Park |

Tony Park |  Helpful Life Stories |

Helpful Life Stories |  RV Samuel's Dad |

RV Samuel's Dad |  TEXAS Fishing Boat |

TEXAS Fishing Boat |  US Regional Information Local News |

US Regional Information Local News |  Hae Naem |

Hae Naem |  good thinking |

good thinking |  Shining Our Own World |

Shining Our Own World |  Full Leaf Flute Edition |

Full Leaf Flute Edition |  Khan Film Blog Production |

Khan Film Blog Production |  Colorado Love |

Colorado Love |  Physical Laws and Science |

Physical Laws and Science |  Pennsylvania Aunt |

Pennsylvania Aunt |  Information Search LifeMAN |

Information Search LifeMAN |  donggul donggul |

donggul donggul |  Vacation on Hawaii |

Vacation on Hawaii |